Silver Back in Triple Digits Overseas as Supply Strains, COMEX Glitch, and Market Turmoil Signal a Structural Bull Run

- Silver Just Completed the Most Volatile Month in Modern History: After surging to an all-time high above $121 per ounce in late January, silver corrected sharply into the $70s before stabilizing near $94 by the end of February. Extreme volatility is not a sign of weakness — it is often the hallmark of a developing commodity supercycle.

- Ten Consecutive Monthly Gains — A Historic First: Despite February’s violent correction, silver still closed higher in U.S. dollar terms — marking its tenth consecutive positive monthly close, the longest streak on record. Sustained momentum of this length historically signals structural, not speculative, demand.

- Gold’s Seven-Month Winning Streak Mirrors 1973: Gold has now posted seven straight positive monthly closes — a run not seen since the early 1970s bull market. Strong gold trends often precede and fuel larger percentage gains in silver.

- The Gold-Silver Ratio Is Breaking Down: The ratio closed near 56, reflecting silver’s recent outperformance. In precious metals bull cycles, falling ratios typically signal growing investor appetite for silver’s higher volatility and upside torque.

- Silver Is Already Back Above $100 in China: When accounting for local premiums, silver in China is trading back in “triple-digit land.” Shanghai Gold Exchange premiums near +15% over Western spot prices show strong physical demand and tightening supply in Eastern markets.

- Physical Inventories Continue to Drain: Industrial-sized 15 kilo silver bars continue flowing out of Chinese exchanges, while COMEX registered and eligible inventories are falling. Tightening visible supply during rising demand conditions is classic bull market fuel.

- India Is Opening the Capital Floodgates: India is allowing actively managed equity funds greater exposure to precious metals and is moving away from London-based pricing benchmarks starting April 2026. Meanwhile, Indian investors just allocated more capital to gold ETFs than to stock funds. This represents potentially billions in new demand entering a relatively small market.

- Institutional Flows Are Accelerating: U.S. gold fund inflows are on pace to surpass last year’s $101 billion. Yet, relative to allocations in equities and bonds, institutional exposure to precious metals remains historically small — suggesting significant room for further capital rotation.

- COMEX Glitch is Undermining Confidence: A February 25 CME Globex outage halted metals trading just as silver surged above $90. The timing has fueled skepticism about paper-market stability and strengthened the case for owning physical bullion rather than relying solely on derivatives exposure.

- Supercycle Dynamics Are Taking Shape: Former Goldman Sachs commodities head Jeff Currie describes the current environment as early-stage supercycle behavior — sharp spikes, violent corrections, and repeated surges driven by supply constraints, de-dollarization, central bank buying, electrification demand, and persistent debt fears. In such cycles, volatility precedes sustained higher highs.

Silver trades back into triple digits in China despite COMEX disruptions, as record monthly momentum, tightening physical supply, rising Eastern premiums, accelerating institutional inflows, geopolitical strain, electrification-driven demand, and deepening skepticism toward paper pricing point not to the end of a spike — but to the early stages of a structural bull market.

From $121 to $93: Volatility, Glitches, and the Bigger Bull Market Picture for Silver

February 2026 will be remembered as one of the most dramatic months in modern silver market history. What looked like a parabolic breakout above $120 per ounce quickly transformed into a violent correction — only to stabilize at levels that still reinforce a powerful long-term bull trend. Beneath the volatility lies a deeper story: tightening physical supply, rising Eastern demand, institutional capital flows, and increasing skepticism toward Western paper pricing mechanisms.

Silver’s Journey: From Record High to Sharp Correction

Silver began its recent surge by reaching an all-time high above $121 per ounce on or around January 29, 2026. The rally was swift and aggressive, driven by intense investment demand and tightening supply dynamics.

But as is common in commodity supercycles, extreme upside momentum was followed by an equally sharp correction. Within days, silver fell below $100, at times dropping into the high $70s and low $80s. Through early and mid-February, volatility remained elevated, with prices fluctuating between roughly $73 and $85.

By the final week of February, however, silver had regained composure. A recovery pushed prices back into the $85–$95 range, ultimately closing the month near $93.79 per ounce.

Despite the gut-wrenching pullback from $121 to $93, silver still marked its tenth consecutive positive monthly close in U.S. dollar terms — the longest monthly winning streak on record. In other words, even after historic volatility, the broader uptrend remains intact.

This kind of behavior — explosive rallies, violent corrections, and quick recoveries — is often characteristic of early-stage commodity supercycles rather than exhausted markets.

The COMEX Glitch and Growing Skepticism

Adding to February’s drama was a significant technical disruption at the CME Group’s Globex platform on February 25, 2026. The outage halted electronic trading across COMEX metals — including gold and silver — for roughly 90 minutes.

The timing raised eyebrows. Silver had been rallying aggressively before the halt, touching intraday highs near $91 per ounce. When trading resumed, prices pulled back toward $88, producing what many described as a “liquidity rupture” during a critical moment of price discovery.

Critics questioned whether the disruption was merely technical or whether it conveniently cooled a market threatening to accelerate into another upside spike. The incident occurred close to First Notice Day for March silver contracts — a sensitive period for physical delivery obligations — intensifying speculation about short-side pressure.

The glitch further undermined confidence in Western paper pricing mechanisms. At a time when physical inventories on COMEX are falling and industrial-sized silver bars continue flowing out of Asian exchanges, market participants are increasingly focused on the divergence between futures trading and physical demand realities.

Meanwhile, China’s silver market has reflected a different dynamic. When accounting for local premiums — recently near +15% over Western spot prices — silver has effectively traded back into triple-digit territory in Chinese markets.

This East-West pricing gap underscores strong regional physical demand and adds fuel to the argument that global bullion markets are gradually localizing price discovery.

India has also announced that beginning April 2026, it will move away from London-based precious metals benchmarks, a significant structural shift in how bullion is priced and referenced globally.

Together, these developments point toward a world in which physical flows and localized pricing mechanisms may play an increasingly dominant role.

David Tait: Debt, Geopolitics, and Structural Support for Gold

David Tait, head of the World Gold Council, recently outlined what he sees as multiple fundamental drivers supporting gold’s continued advance — dynamics that often spill over into silver.

- Among the key forces he cited:

- Persistent geopolitical instability

- Central bank buying averaging around 1,000 tons annually in recent years

- Expanding access to gold investment vehicles in markets like China and India

- A structural fear of runaway sovereign debt

Tait emphasized that debt sustainability fears — particularly following moments of stress in U.S. bond markets — have become a core underlying driver of precious metals demand. In his view, the global debt trajectory shows little sign of reversal, reinforcing the long-term case for bullion ownership.

For silver investors, gold’s macro foundation matters. Historically, sustained gold bull markets create the monetary and psychological backdrop for silver’s more explosive percentage gains.

Jeff Currie: Classic Supercycle Behavior

Former Goldman Sachs Head of Commodities Jeff Currie characterized the recent volatility in gold and silver as typical supercycle behavior rather than a sign of exhaustion.

Currie explained that in supply-constrained environments, prices often surge as demand overwhelms available inventory. When prices spike too quickly, demand temporarily collapses, triggering sharp corrections. Then buyers re-enter as prices look attractive, reigniting the cycle.

In silver’s case, he described it as a “turbocharged version of gold” — sharing precious metal monetary characteristics while also serving as a critical industrial input for electrification, solar panels, and advanced electronics.

Currie also pointed to:

- De-dollarization by central banks

- Portfolio underinvestment in metals

- Structural industrial demand growth

These forces, combined with silver’s relatively small market size, mean incremental capital flows can produce outsized price movements.

Conculsion

The February plunge from $121 to $93 was dramatic. But zooming out, silver remains in a historic monthly uptrend, physical inventories are tightening, Eastern markets are showing premium-driven strength, and institutional capital flows are accelerating.

Layer onto that a CME trading disruption that dented confidence in paper markets, growing debt fears voiced by global bullion leaders, and supercycle dynamics described by seasoned commodity veterans — and the picture becomes clearer.

Volatility is not the end of the story. It may well be the defining feature of the early innings of a structural bull market in silver.

Weekly Market Update Notes by James Anderson

The silver and gold markets finished this week and month on a strong note.

The silver spot price ended the week at $93.79 oz bid.

The spot gold price closed the week basically flat at $5279 oz bid.

The spot gold silver ratio fell to close the week at 56.

Gold closed this month of February 2026 with strength, marking a seventh positive monthly close candle; you have to go back to 1973's run to find a monthly run of positive spot price appreciation of that length.

Even with last month's large price selloff in silver, the white precious metal closed this month up in fiat US dollar terms for the tenth month in a row. The longest monthly streak on record for silver.

Silver closed trading in China this week already back in triple-digit-landia when their local price premiums are converted into fiat US dollar terms.

Their respective palladium and platinum bullion pricing to close their trading weeks were both multi-hundreds of dollars per troy ounce higher than the Western world spot price feeds closed this week.

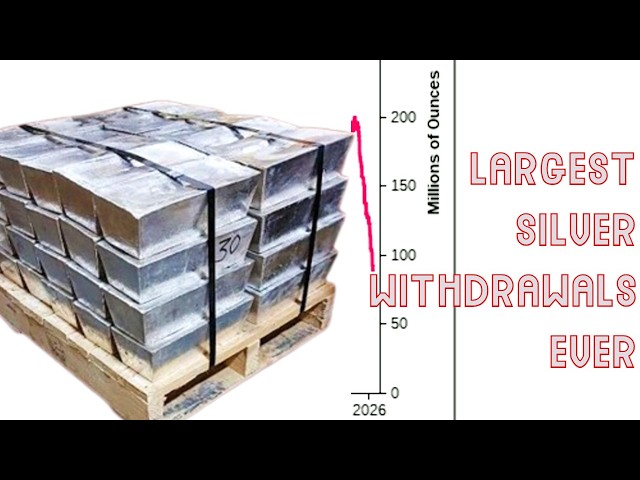

You can see the SGE silver premiums reverted higher this week, with the blue line reflecting local premiums near +15% higher than price quotes in the Western world.

Silver bullion industrial sized 15 kilo bars continue flowing out of their SGE and SHFE exchanges now down to a combined 24.59 million oz to close this week.

India made big news in the gold and silver bullion markets this week with a few important headlines.

India's market regulator is going to allow a large percentage of their nation's actively managed equity funds to put more capital to work in the precious metals sector.

This move opens the potential for billions further of Indian investments to go chasing limited piles of gold and silver within their investment and ETF system.

This past month Jan 2026, Indian investors put more money into Gold ETFs than into stock funds.

India also announced that come April 2026, their local market will no longer use precious metals price data or price benchmarks out of London or the associated LBMA.

Bank of America published this chart using year to date golf flow data tracking US fund flows to gold thus far near now two months into this year.

At this pace Western institutional investors will break last year's $101 billion gold net long bet flow.

Let me remind you how tiny institutional US investment managers' collective gold fund flows have been first half of this decade through last year 2025, when compared to how much capital they put to work in underperforming bonds, cash, and general equities or US stocks.

Just a general lookup using Google Trends in USA and you can see the public at large is also getting in on the risen buy gold and buy silver bullion trends.

Stick around, on the other side of this short break, we're going to look at the second CME COMEX Silver futures trading 'technical issue' which hit the market middle of this past week.

Adding to further evidence as to why India and China are bringing their respective precious metals markets into localized price feeds as Western world price shenanigans continue occurring on a regular ongoing basis. This week's folly just that latest example.

Let's check in with India's CNBC TV-18's Manisha Gupta who spoke with the head of the World Gold Council this past week in the world's second largest gold buying market.

If you were paying attention to price action and headlines this week you probably saw disgust for another COMEX precious metals futures technical glitch that knocked price feeds offline for around an hour and a half.

Where likely which ever entities were caught painfully short and underwater on their short side trading were able to wiggle out a reported 159 million oz notional trading block coming down to the end of the month, with a falling silver price thanks in large part to the backroom glitch saving the alleged losing parties hundreds of millions in potential losses had that glitch and price markdown not occurred.

Thoughts immediately reverted back to the Thanksgiving CME cooling issue silver price meltdown, and the positive price action that followed shortly thereafter.

I'll leave a link to the CME Group's X post announcing the glitch so you can see the over one thousand cynical responses they received.

Faith in these derivative commodity price market makers has been driven further lower.

We even got some decent silver round mock-ups to celebrate this week's clown show.

On the COMEX Silver warehouse registered and eligible supply side, both piles continued falling this week.

Turning to former Goldman Sachs Head of Commodities, Jeff Currie went on the MacroVoices podcast this week and banged the table on both gold and silver.

His recent comments are worth hearing regarding both precious metals.

Tavi Costa's chart here to close this week give you a longer term view of the bullion bull market we are building.

Gold's above ground value divided by the world's total stock market value in gold bull market cycles often screams back towards parity, and as you can see we are just getting underway.

That will be all for this week's Bullion Market Update.

Sources:

Rising Bharat Summit 2026 LIVE: David Tait Explains What's Driving Surge In Gold Prices

https://www.youtube.com/watch?v=WectpSTcj9U

CME Group's COMEX Silver Price Glitch X Post Responses, Are Worth a Look:

https://x.com/CMEGroup/status/2026738200731918752

MacroVoices #521 Jeff Currie: The Great Rotation

https://youtu.be/uhpECa_XaBA?si=TrUYk1Zg81comdUT&t=1811

Bank of America Predicted Silver Prices Could Hit $309 in 2026. Is That Still in Play?

https://finance.yahoo.com/news/bank-america-predicted-silver-prices-123002375.html