Was the Gold and Silver Bottom In? Bullion Market Outlook Discussion

- Gold and Silver Show Resilience Amid Volatility: Precious metals experienced a sharp selloff before recovering on renewed Middle East peace-deal speculation. Gold ended the week at approximately $4,219/oz, while silver closed near $68.02/oz.

- Market Timing Remains Uncertain: The report cautions investors against trying to identify an exact bottom in silver and gold prices, arguing that market turning points are only obvious in hindsight.

- U.S. Fiscal Deficits Continue to Expand: Federal overspending approached $300 billion for the month, with the U.S. projected to exceed a $2 trillion budget deficit this fiscal year, adding pressure to long-term debt sustainability.

- Debt Servicing Costs Are Becoming a Major Concern: Interest payments on U.S. government debt are now approaching military spending levels, highlighting growing fiscal strain and raising questions about future monetary policy flexibility.

- Global Currency Creation Supports the Gold and Silver Bullion Case: Worldwide fiat currency supply expanded by more than $7 trillion between December 2025 and April 2026, reinforcing the report's long-term bullish outlook for precious metals as stores of value.

- Gold Bull Market Viewed as Consolidating, Not Ending: Analysts featured in the update compare the current correction to a pause during a broader climb higher, suggesting gold may test lower levels before resuming its long-term uptrend.

- Central Banks Remain Key Gold Buyers: Market commentators emphasize that central bank demand continues to underpin gold prices, while investor demand is expected to return as economic and financial risks become more apparent.

- Equity Valuations and AI Spending Face Scrutiny: The report highlights concerns that stock market valuations and the AI investment boom may have become excessive, drawing comparisons to previous technology and infrastructure bubbles.

- Silver Supply Constraints Are Intensifying: Global silver mine production has stagnated for nearly a decade, while rising sulfur costs and Chinese export restrictions are creating additional challenges for silver refiners and miners worldwide.

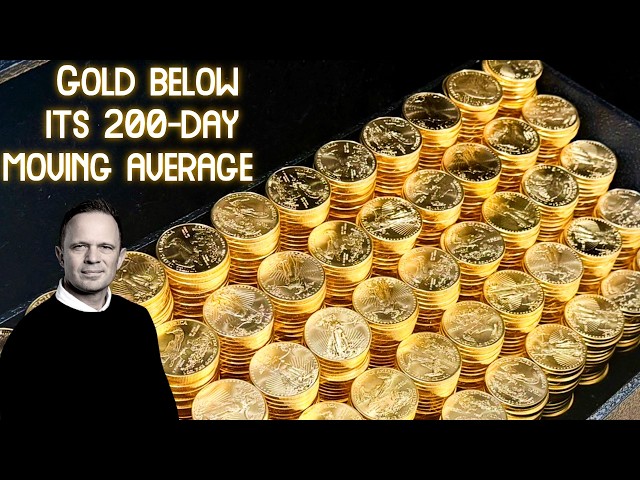

- Bullion Advocates See Current Prices as a Buying Opportunity: With both gold and silver trading near or below their respective 200-day moving averages, the report argues that the current correction presents an attractive entry point for long-term precious metals investors.

With gold and silver trading near key technical levels, market experts argue that current weakness may represent a buying opportunity rather than the end of the precious metals bull market.

Last Week's Gold and Silver Market Update:

- The precious metals market sold off and then rallied back on peace rumor news.

- The spot silver price slightly up closed at $68.02 oz bid.

- The spot gold price fell over all to close the week at $4,219 oz bid.

- The spot gold silver ratio fell lower higher to close the week at 62.

I entitled this week's update as a reminder to any of you out there. The exact numbers, path and timeline of this price correction's bottoms, only omniscience knows. It's kind of like when is the Trump administration and Iran going to come to terms on a peace deal?

Perhaps we'll only know it once you have fully seen it fully in the rearview.

Meanwhile nominally ramping the US stock market perhaps cynically for rounds of corporate insider IPO bag dumping onto retail.

Since 2006, the largest 20 IPOs by market cap saw drawdowns on average of -61% only one year later.

Ignoring the silly hyperbolic language of bot articles saying things like silver surging over $67 oz.

This week we got nearly the 40th promise of an Iranian peace deal, with another rising gov't inflation print of 4.2%

Anyone trying to stay cool or actually transporting anything in the real world, knows is an insult recent experiences.

Almost $300 billion in Federal gov't overspending for last month.

The feds are well on their way to another over $2 trillion budget deficit this fiscal year.

Happy coming birthday USA, I'm not even going to mention the unfunded liabilities multiple larger than these ballooning debts to come.

Interest on our debt is already at our near military spending which is hard to deduce given new wars we've engaged.

Foreign US bond holders continue selling our debt on net thanks to increases in energy prices the world over ($150 billion or so since the war started).

Perhaps some of that ended up on a the fiat Fed's balance sheet which has gone from light QT to now again expansion since the start of the year 2026.

Heads up next week Thursday for new Fed head Kevin Warsh's policy talking points. It seems both US Banks and stablecoins will have to pick up shrinking foreign US debt buyers.

The good news for now remains that internationally the fiat US dollar is still dominate and it can increasingly afford us more bullion than is did earlier this year. Later this decade into next, I doubt we will be able to make either claim.

Fiat currency creation around the world from December 2025 through the end of April 2026 (5 months) is up over $7 trillion. Annualize that growth, and we're talking low double digit percentage growth what most people misnamed money long ago.

If we stopped creating fiat currency (and you know that won't happen anytime soon), the price of the world's physical gold pile still needs to double to reach the old 40% coverage levels hit in the early 1980s. And yes this fiat M3 pile will undoubtedly grow more along with myriad stable coin gov't debt financing schemes coming.

Here was Ronnie Stoefelle of In Gold We Trust Report talking about the likely road for gold through the end of this decade.

You have seen this chart before, illustrating on a relative basis how much larger gold ETF holdings were in the 2011 bull market top vs where they have been since. Even unsecured gold proxies are hardly owned relative to other ETF bubble asset piles.

This chart made the round this week, highlighting that the last few years of large unsecured gold ETF buying from $2300 oz onward was more than 1/3 done by Asian investors (mainly in China). This bullion bull doesn't end until Western investors also too go ankle deep into precious metals allocations. Most Western investors have near none still, much less any clue that 110 million oz of supposed gold in ETFs is only like 1.5% of all the gold we have ever mined. They are a sentiment indicator, unlike silver ETF flows which can literally through that market into price ramps and declines as we have recently seen over the last year or so.

Finishing this first half with famed Indian gold research analysts at Yardeni Research. As you can see, gold blew outside their red forecast lines to start the year, we're now getting an opportunity to buy on the other side of the climbing pattern.

More Gold Silver related price action charts ahead, plus some recent thought leader insights, from even Mr. 60, 20, 20 gold portfolio allocation bullion bull himself. We'll be right back.

As you likely know, world silver production from miners has been stagnant for the last near decade running. The world is increasingly relying on secondary recycled silver supplies to make ends meet.

A major problem for large silver miners using sulfur in zinc refining for instance is the exploding costs of sulfur if you can secure supplies. Over 1 in 8 ounces of world yearly mined silver comes from Chinese zinc refining which requires heavy loads of sulfer they banned from exporting last month.

We are seeing many reports from some of the largest silver miners in the world that their outputs are not keep up with the last few years. I'm not just talking about China, but also the largest mining market in the world Mexico.

The gold price is now well below its ongoing 200 day moving average now near $4,450 oz. In bullion bull markets, this is buying season. 200 days ago the price of gold was just below $4100 oz and thus in the coming months the 200 day moving average will keep rising given gold's Q1 2026 move. The point is gold is now on sale.

200 days ago silver was still priced near its seemingly ancient resistance of $50 oz. The current 200 day moving average is near $68 oz but that average will be rising into the $70s oz and higher given silver's spectacular move last Dec and Jan. So yes silver at and below its 200 day moving average is also now available for bullion bulls.

Moving on to hear from David McAlvany whose coming take is much in line with what we have covered.

Finally Mr. 60, 20, 20 gold portfolio allocation shot caller, Mike Wilson CIO of Morgan Stanley was interviewed this week.

He spoke about hot capital flows injecting unsustainable moves from commodity to commodity sector, gold and silver explicitly mentioned. Have a listen.

That is going to be all for this week's bullion market update.

Sources:

Why the momentum for gold is shifting (BNN Bloomberg interviewing David McAlvany )

https://www.youtube.com/watch?v=hgz0X6fm2pI

60 / 20 / 20 Portfolio fame: Mike Wilson CIO at Morgan Stanley

https://youtu.be/GkivojhIz2w?si=tyfRc63RWMsB0zbi&t=70

Mike Wilson on unsustainable rates of change & hot momentum traders running from one sector to another

https://youtu.be/FohlEakgBR8?si=3K1Nc4hbAZ4GKHmP&t=150